This finance guide teaches the basic rules of finance for beginners. You will learn about taxes and the savings accounts that give you a boost to grow.

Understanding these tips serves both new residents and young people who should always apply finance for beginners to better control their money. In this way, they increase their credit and improve their lives.

What would you like to explore?

Choose a category to review available credit card options and information.

This plan shows the right way to escape inflation. Thus, it ensures that money does not lose value and builds a better life in the country.

10 Golden Rules for Financial Control Today

1. Know Where Your Money Is (Finance for beginners)

To organize your financial life, first calculate how much money you have and what you owe. This calculation helps create urgent plans, such as paying off your credit card, and goals for the future, such as retirement.

Knowing where you are now avoids lost expenses and ensures that your choices have a clear objective.

2. Separate What You Need from What You Want

To control your spending, separate what is essential (need, such as housing and medicine) from what is superfluous (want, such as travel and luxury). This separation changes. A car, for example, is a want if there is a bus nearby. But it becomes a need in isolated places. Use the budget planner from the Financial Consumer Agency of Canada (FCAC) to compare your spending with the national average.

3. Tackle the Most Expensive Debts Now (Finance for beginners)

Short-term debts, especially credit card revolving credit, charge higher interest rates than capital market returns.

Eliminating these liabilities generates savings equivalent to the interest that would be paid to the institution.

Obtaining debt consolidation with lower rates helps those facing critical indebtedness.

4. Build Your Emergency Fund and Protect Your Money

Having an emergency fund protects your money. It prevents you from needing to sell your things in a hurry during difficult times.

Thus, if you have a steady job, save the equivalent of 3 to 6 months of your basic bills.

Now, if you work for yourself, do side gigs, or live in expensive cities, try to save the equivalent of 6 to 12 months.

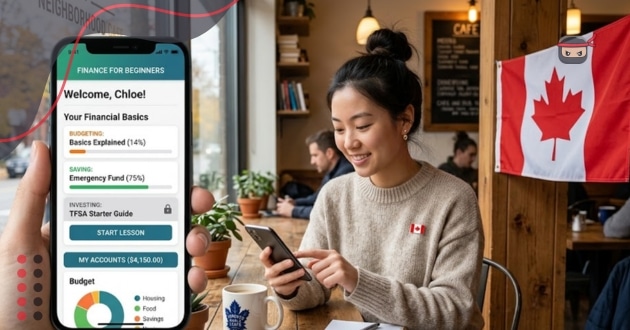

5. TFSA and RRSP Accounts: Save and Pay Less Tax

With a TFSA account, you take out your money without paying any tax, no matter what you use it for.

Already the RRSP plan helps to pay less tax now, as the government deducts the amount you save.

In these two cases, you only pay this tax down the road, when you retire and your income is lower.

6. Use the FHSA and Buy Your First Home (Finance for beginners)

The First Home Savings Account (FHSA) is the best help for those dreaming of having their first property.

The FHSA combines two great advantages for your pocket:

- You deduct the tax from the money you put into the account.

- Later, you take out the amount without paying tax.

You can also use the FHSA along with the Home Buyers’ Plan (HBP) from the RRSP. Thus, you save up a good amount of money, tax-free, to pay the down payment on your house or apartment.

7. Keep Your Name Clear and Your Score High

Your credit score (calculated by Equifax and TransUnion) decides the interest on loans and financing.

Always pay your bills on the right date! This shows that you are responsible. Even in a crisis, pay at least the minimum.

Use less than 30% of your total credit limit. This makes your score go up.

8. Save Money Automatically (Finance for beginners)

Schedule the transfer from your account to savings as soon as you get paid. This saves your money before you spend it on things you don’t need.

The automatic system takes the part of saving out of your daily thoughts and ensures you reach your goal.

9. Use Government Benefits to Have More Money

The government returns money to those who file their income tax return in detail.

In it, you pay less tax or receive more back when you use the right accounts (such as pension accounts) and declare important expenses, such as medical or study expenses.

Take this money back and put it straight into your savings accounts.

10. Review Your Bills and Save (Finance for beginners)

Forgotten subscriptions and repeated insurance steal your money. Once a year, call the internet and phone companies to negotiate lower prices.

We recommend that you compare insurance values and cancel what you don’t use to make your money go further.

7-Step Plan for Those Who Want to Change Their Life

- Get Your Document and Open Bank Accounts. First, you need a Social Insurance Number (SIN) to work legally. With the SIN in hand, go to a reliable bank and open a checking account and a savings account. This is the basic requirement to receive your salary and start saving money.

- See How Much You Have and How Much You Owe. Make a list of all your money and all your debts. This record of your pocket shows where you are starting from and helps you see if, over time, you are improving your life.

- Track Every Cent You Spend (for 30 or 60 days). Monitor all your spending for one or two months. Note everything: from rent to small daily snacks. Doing this tracking shows where the money is leaking and helps you create spending limits that work in real life.

- Use All Your Surplus to Pay Off Expensive Debts. Take any money left over and use it to settle credit cards and other debts with high interest rates (above 20% per year). Getting rid of these debts is the best investment you can make.

- Set Up Protection Against Unexpected Events. Keep your emergency fund in a savings account that pays good interest (HISA) or in funds that do not lose value. The focus is to keep your money safe, so you can withdraw it quickly if something urgent happens.

- Open Accounts That Reduce Your Taxes. After having the reserve, open special accounts like TFSA, RRSP or FHSA. Use the money saved in them to buy simple assets, like market-following funds (ETFs) or safe bonds.

- Invest Little by Little Automatically. To start investing, take a simple test and see how much you are willing to lose if the market falls. With the result, start applying money automatically and constantly.

Technological Tools for Budget Management

1. Monarch Money (Finance for beginners)

Monarch Money gathers your balances and investments from various banks in one screen.

This app shows how much money you have in total without you needing to record anything by hand.

Furthermore, the downside is that the connection with the bank can fail and stop updating the data automatically.

2. You Need A Budget (YNAB)

The YNAB is a simple rule: you only spend the money you already have in hand.

It is relevant to know that the system forces you to divide every cent that entered among your bills, savings, and what you need to pay later.

This method requires you to look at your expenses every day, but soon breaks the trap of depending on the next paycheck.

KOHO

KOHO offers an account for everyday life with a Mastercard and savings.

It helps those who just arrived in the country to create a good credit history without risks.

The app also gives back part of the money spent on common purchases and facilitates your banking life.

Conclusion

Organize your expenses, use tax benefits, and build your credit. These actions protect your money and make you reach your goals faster.

With the correct organization, you avoid expensive fines and abusive interest. Understand how money works in Canada to have stability and long-term freedom.

Don’t waste time. Download the Canadian government’s budget planner. Start recording your expenses today and change your financial life.

Even in the short term, it is possible to have good returns. If you want to save and already start having good financial results, see now the best investments for short term goals.